Brokers that combine equities, equity options, and futures in one account, under one margin engine, match how active derivatives clients now trade. Unfortunately, only few platforms currently deliver that combination. Most vendors specialize in one or two asset classes, leaving brokers to stitch together separate stacks per asset class, then explain to clients why their P&L, positions, margin, and risk views live in different places. The cost of that fragmentation has risen as retail traders move between SPY 0DTE, micro E-mini futures, single-stock options, and short-dated ETF options in the same session.

This article addresses why a unified equities, futures, and equity options trading platform such as DXtrade is almost a unique offering on the market, what strategies clients want to run, what the technology underneath has to handle (OMS routing, SPAN margin, leg validation, fill logic), and where the regulatory boundaries sit.

The retail derivatives flywheel keeps accelerating

CME Group closed 2025 with a record average daily volume of 28.1 million contracts, up 6% on a 2024 that was itself the best year in the exchange’s history. Micro E-mini equity index futures and options reached 2.8 million ADV, around 40% of all CME equity index volume, with Q1 2025 alone bringing in 83,000 new retail clients, up 44% year over year. ICE traded a record 2 billion futures and options contracts in 2024 and another 1.2 billion in the first half of 2025. The U.S. listed options market is on track for a sixth consecutive record year at roughly 13.8 billion contracts.

Inside that growth, short-dated options now drive a large share of the order flow. SPX zero-day-to-expiration contracts hit 62.4% of total SPX volume in August 2025, a market-wide signal that short-dated demand has become the norm rather than the exception. The same shortening-tenor pattern shows up in single-stock options and in ETF options on SPY, QQQ, and IWM. Cboe’s Henry Schwartz noted that an expected leveling-off of growth in short-term options has yet to happen.

The retail trader generating this volume is not the trader of five years ago. WEF and BCG’s 2024 Global Retail Investor Outlook found that 20% of Gen Z investors hold derivatives, against 7% of Boomers. Robinhood’s late-January 2025 rollout of index options to all U.S. customers, followed by its CME futures launch, was directly cited by Cboe as the trigger for the February 2025 SPX 0DTE share spike. When Robinhood’s chief brokerage officer Steve Quirk launched Robinhood Legend, he framed the build around frustration with legacy offerings. Brokers that cannot serve clients hopping between an iron condor on SPY, a long ES futures position, an AAPL covered call, and a CL crude calendar spread inside one session lose those clients to brokers that can.

Why combining is more valuable than offering a single feature

Brokers historically picked a side. Futures specialists built around DOM ladders, FCM clearing, SPAN margining, and exchange-native spread types. Equity options brokers built around chains, strategy templates, Reg-T margining, and portfolio-margin tiers. Cross-asset retail clients learned to live with two logins. The economics of that arrangement now break down on four fronts:

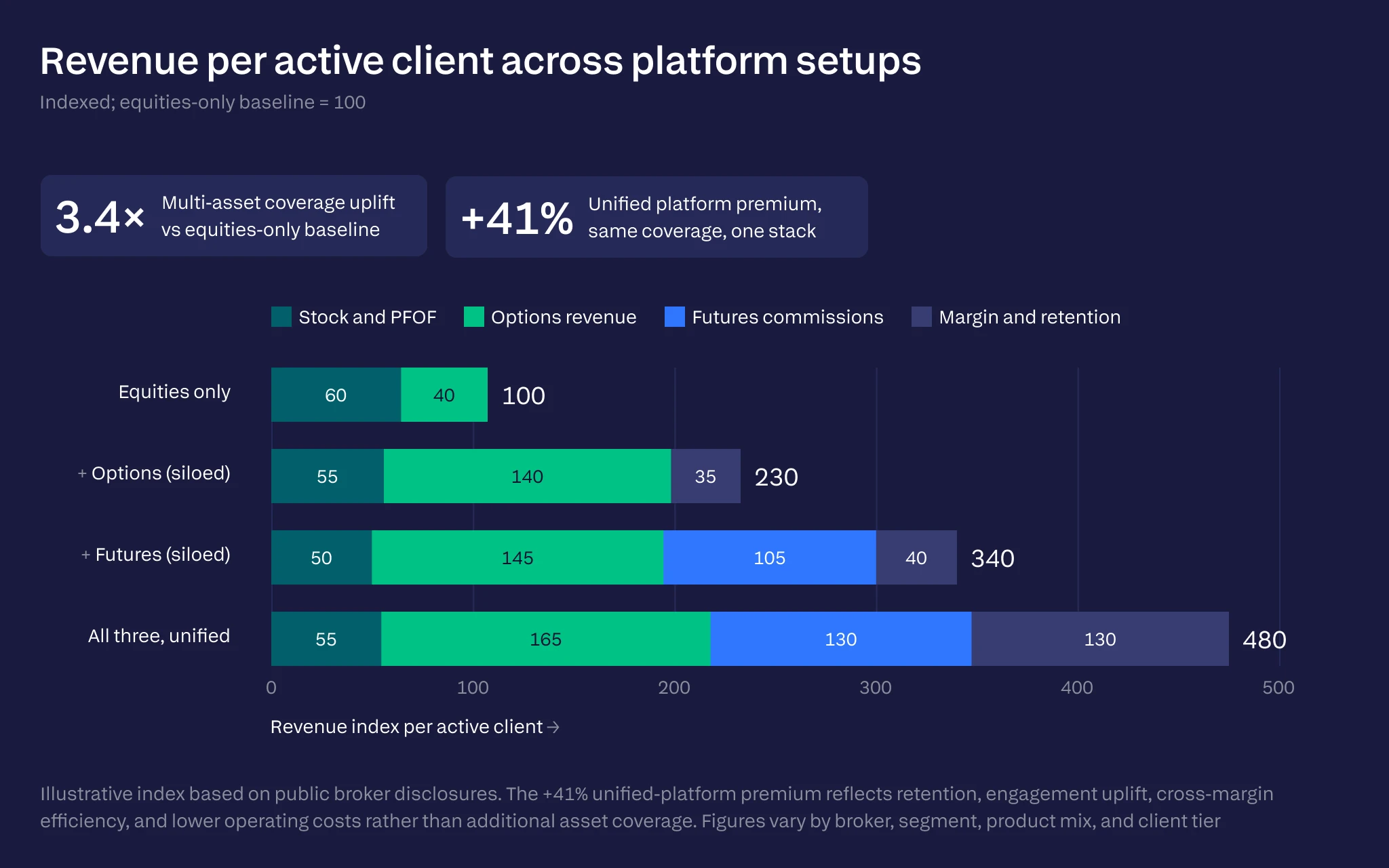

- Wallet share. A trader who keeps a futures account at one venue and an options account at another routes incremental dollars to whichever side feels more cohesive.

- Margin efficiency. CME’s portfolio-margining program saved customers a record $8.4 billion of margin a day on average across 2025, signaling how much capital efficiency cross-product offsets unlock at the clearinghouse level. The same logic applies on the broker side: a unified platform that runs Reg-T strategy offsets, OCC TIMS portfolio margin for qualifying equity-options accounts, and a single buying-power view across the securities side and futures lets clients deploy capital more efficiently than two disconnected accounts ever could.

- Operational risk. A 0DTE assignment cycle running across two disconnected systems produces the reconciliation gaps that show up as wrong-way positions on Monday morning.

- Supervision overhead. Compliance, risk reporting, trade surveillance, and client statements run twice when positions sit in two systems, and the gap between them is where errors hide.

The Acuiti CFD broker survey found that 89% of CFD brokers ranked regulatory compliance as their top operational challenge, and many are now expanding into listed futures and equity options to diversify away from CFD-only revenue. Adding listed F&O on top of an existing CFD or equities stack has historically required a parallel build, which most CFD brokers cannot resource against an already-stretched compliance budget. Vendors that solve this without a parallel build cut a 12-to-18-month integration to a launch in weeks.

Strategies clients want to run, and why platforms break

Client orders follow payoff shape across asset classes. The strategies that drive engaged retail and prop flow run across the securities side and futures, and a serious platform must support each as a single ticket with correct margin and lifecycle handling.

Covered calls, protective puts, and collars

A covered call pairs long stock with a short OTM call to harvest premium and cap the upside. A trader long 100 shares of AAPL sells an out-of-the-money AAPL call and pockets the premium. A protective put does the inverse, pairing long stock with a long OTM put to cap downside at strike minus premium. A collar combines the two, defining a price corridor at near-zero net premium. Each of these is economically a single position. Reg-T strategy margin treats them that way, recognizing the offset between the underlying and the option leg. A platform that books the stock on one ledger and the option on another, however, computes margin twice and either over-collateralizes the client or under-recognizes the offset.

Verticals, straddles, strangles, and ratio spreads

Vertical spreads define max gain and max loss with two same-expiration options at different strikes. Straddles and strangles express volatility views, one with same-strike calls and puts, the other with OTM strikes. Ratio spreads adjust leg counts to skew the payoff. Each maps to a Cboe Complex Order Book strategy with strategy-specific Reg-T treatment that differs sharply from naked-leg margin. The platform has to recognize the structure pre-trade and apply the correct margin formula on fill.

Calendar spreads and iron condors

Calendar spreads exploit differential time decay between a long longer-dated option and a short shorter-dated option at the same strike. Iron condors combine a short OTM call spread with a short OTM put spread, four legs in one structure. Butterflies require a 1:2:1 ratio in lowest terms, enforced by exchange validation. On the futures side, calendar spreads between contract months carry their own treatment under SPAN’s intra-commodity spread charge, often producing margin a fraction of two outright positions, while exchange-native multi-leg order types route through CME Globex User-Defined Spreads with guaranteed simultaneous fills. Traders abandon these structures at order entry whenever their platform fails to validate the ratio, route the legs atomically, hold a defined margin against the structure, or carry the position cleanly through to expiry.

Synthetic positions and cross-asset delta hedging

A synthetic long combines a long call and a short put at the same strike and expiration, replicating the underlying with a delta near +1. Synthetic positions let traders express directional views, finance long exposure, arbitrage carry against the underlying, or replicate restricted underlyings.

Delta hedging is where futures and equity options meet most directly. An options book on SPY or single names accumulates Δ as the market moves, and the cleanest hedge is index futures: ES for S&P 500 exposure, NQ for Nasdaq, YM for Dow, RTY for Russell. Futures offer leverage, near-twenty-four-hour access, lower capital requirements than the equivalent stock basket, and tighter spreads at index level. A trader running an iron condor on SPY while keeping a short ES position to neutralize gamma needs both books visible in one position keeper, with one combined risk picture. The same logic applies to single-stock options market makers using sector or index futures to hedge beta exposure. None of that workflow is feasible if futures and options sit in separate platforms.

The deeper analytics layer (DOM ladders, vol surfaces, live Greeks, screeners) determines whether traders can construct these positions efficiently. We’ve written about this in detail in our piece on advanced analytics in futures and options trading platforms, which sets out why heatmaps, option chains with full Greeks, integrated screeners, and live volatility surfaces are now baseline expectations.

The technical work behind a unified futures and options platform

Underneath the chain view sits a stack of decisions about order management, leg execution, margin computation, and lifecycle handling that most platforms get wrong because they only have to solve them for one asset class at a time.

Order management and multi-leg routing

A unified OMS abstracts orders into a canonical representation regardless of asset class, then dispatches them through the right gateway. Futures route through CME iLink or ICE iMpact to a single matching engine per contract. Equity options route through a smart order router across 16-plus OCC-cleared venues, obeying the Options Linkage Plan and exchange-specific complex order books. Equities follow Reg NMS. The OMS, therefore, needs different routing layers per asset class but a single account ledger, position keeper, risk feed, and reporting layer.

Multi-leg order types and fill logic

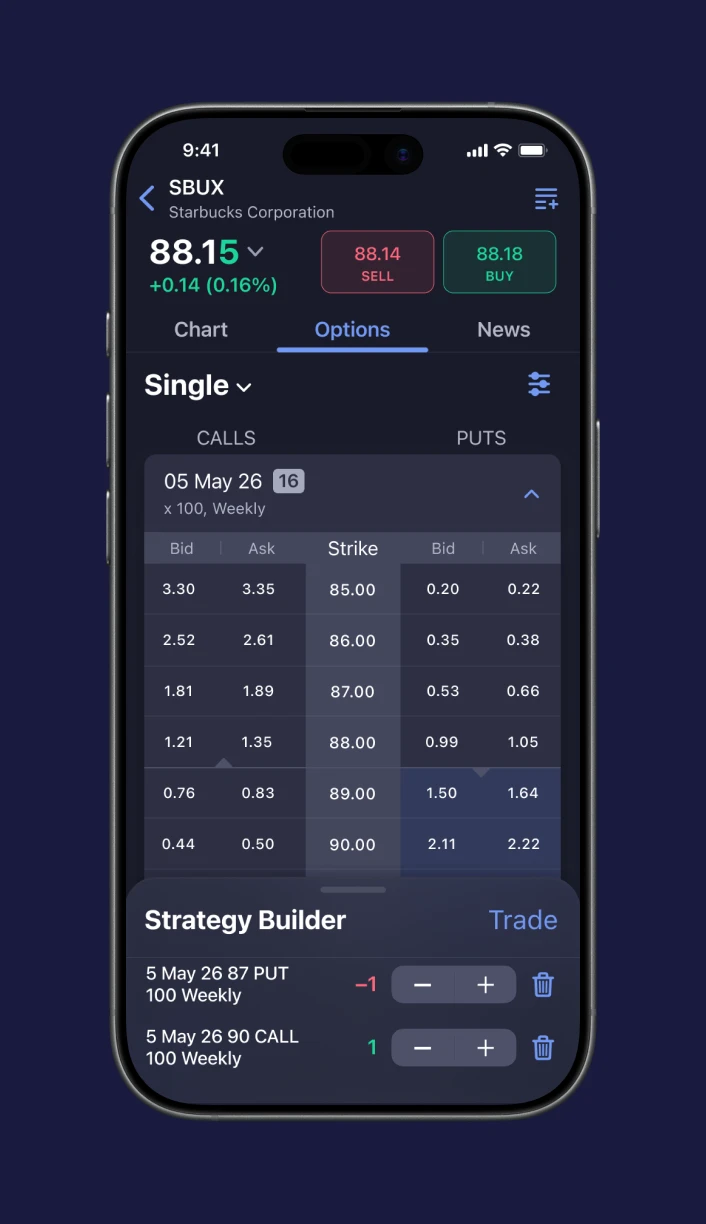

Multi-leg orders come in two flavors. Exchange-native structures trade as a single instrument: CME Globex User-Defined Spreads support up to 40 outright legs, with the matching engine guaranteeing simultaneous fills at exchange-assigned leg prices through SLEDS. There is no leg risk. Cboe’s Complex Order Book offers the same atomicity for equity options strategies. Synthetic legging decomposes the spread and works individual legs, used when no listed structure exists or the spread crosses asset classes. Synthetic legging carries leg risk, the unhedged exposure that opens when one leg fills before the hedge does, and managing it requires a colocated strategy engine, lean rules, post-hedge logic, and timeout policies that close out partial positions before they drift.

Leg validation has to happen pre-trade. A vertical spread requires same expiration, same option type, different strikes, and consistent multipliers. A butterfly’s ratios must be in lowest terms. GTD orders cannot survive past the earliest-expiring leg. The OMS rejects malformed structures before they ever hit the exchange, then performs notional, Greeks, buying-power, and self-match checks on top. Fill logic for atomic spreads is straightforward: the spread either trades or does not. For working legs, partial fills are normal, and the OMS must track each leg’s order ID independently, hedge filled legs against unfilled ones, cancel the residual if the lean breaks, and reconcile the partial position into the parent strategy.

Margin engines: SPAN, SPAN 2, Reg-T, and portfolio margin

Four distinct methodologies coexist for the combined securities-and-futures stack:

- SPAN, the CME 1988-vintage scenario engine used by 50-plus exchanges and CCPs, runs a 16-scenario stress test per contract and aggregates positions into Combined Commodities, with intra-commodity spread charges, inter-commodity spread credits, spot-month delivery charges, and a short-option minimum applied to the result.

- SPAN 2 replaces that with filtered historical VaR drawing on at least ten years of scenarios, plus stress VaR, valuation uncertainty margin, a liquidity charge, and a concentration charge. Long and short positions can have asymmetric margins, breaking pre-trade checks that assumed symmetry. Energy and equity products are live; agricultural and rates products migrate through 2025 and beyond. Calculation latency runs 50 milliseconds to seconds, which is why platforms use CME’s Approximation Service for sub-50ms pre-trade buying-power.

- Reg-T strategy margin under FINRA Rule 4210 governs retail equity-options accounts, with position-by-position formulas (50% on long stock, defined-loss treatment on debit spreads, strike-differential-minus-credit on short credit spreads, and recognized strategy offsets for covered calls, collars, condors, and butterflies).

- Portfolio margin (OCC TIMS) applies to qualifying customers above the $100,000 to $150,000 thresholds, stress-testing equity-options portfolios at ±15% with implied-vol shocks of ±150%, and at ±8% with ±75% vol shocks for broad-based indexes. The capital efficiency versus Reg-T can be substantial for spread-heavy traders.

A platform supporting cross-asset margin across futures and the securities side has to run SPAN or SPAN 2 continuously on the futures-account side, run TIMS or Reg-T on the securities side, present the combined buying power to the trader in one view, and prevent orders that violate either. Pre-trade margin validation, continuous margin recalculation, intraday exposure monitoring, and configurable liquidation triggers are baseline requirements, not premium add-ons.

Symbology and reference data across asset classes

Each asset class lives in its own symbol universe. Globex uses hierarchical futures product codes (ES for E-mini S&P, NQ for Nasdaq, ZC for corn, CL for crude) with single-letter month codes (H, M, U, Z) that the platform has to roll forward as front-month contracts expire. OCC’s OSI uses a 21-character format combining a six-character underlying, expiration date, call-or-put indicator, and strike encoded in 5+3 digits. Equity tickers are simple, but corporate actions trigger OCC adjustment memos that force platforms to manage adjusted option series alongside the standard chain. A unified platform maintains all three universes with cross-reference tables at the FIX boundary, and breaks have to resolve gracefully across corporate actions, futures contract rolls, mid-week expiries, and split-adjusted option series.

Position netting and the regulatory boundary

Position netting works inside an asset class but stops at the regulatory line. Customer cash for futures sits in CFTC Reg 1.20 segregated accounts at a futures commission merchant. Customer cash for equities and equity options sits in SIPC-protected accounts at a broker-dealer. They cannot be commingled, which is why every retail broker offering both runs two legal entities and why customer-level portfolio margin spanning futures and securities remains constrained.

The CME-OCC cross-margining program, restated most recently in 2020, covers clearing-member proprietary accounts and a small set of market professionals, not retail customer accounts. CME’s December 2025 commentary makes the point directly: retail holders of SPX equity options plus ES futures see them margined separately unless they are permissioned for the cross-margining facility. The implication for product design is clear. Even where the clearinghouse limits customer-level offsets, a unified platform still gives the trader a single view, a single risk picture, consolidated reporting, and operational efficiency, and pre-trade buying-power calculations can recognize netting on the broker side. The structural shift toward 0DTE options puts the most pressure on this part of the architecture, a trend covered in detail in this analysis of the 0DTE options surge and its technology implications.

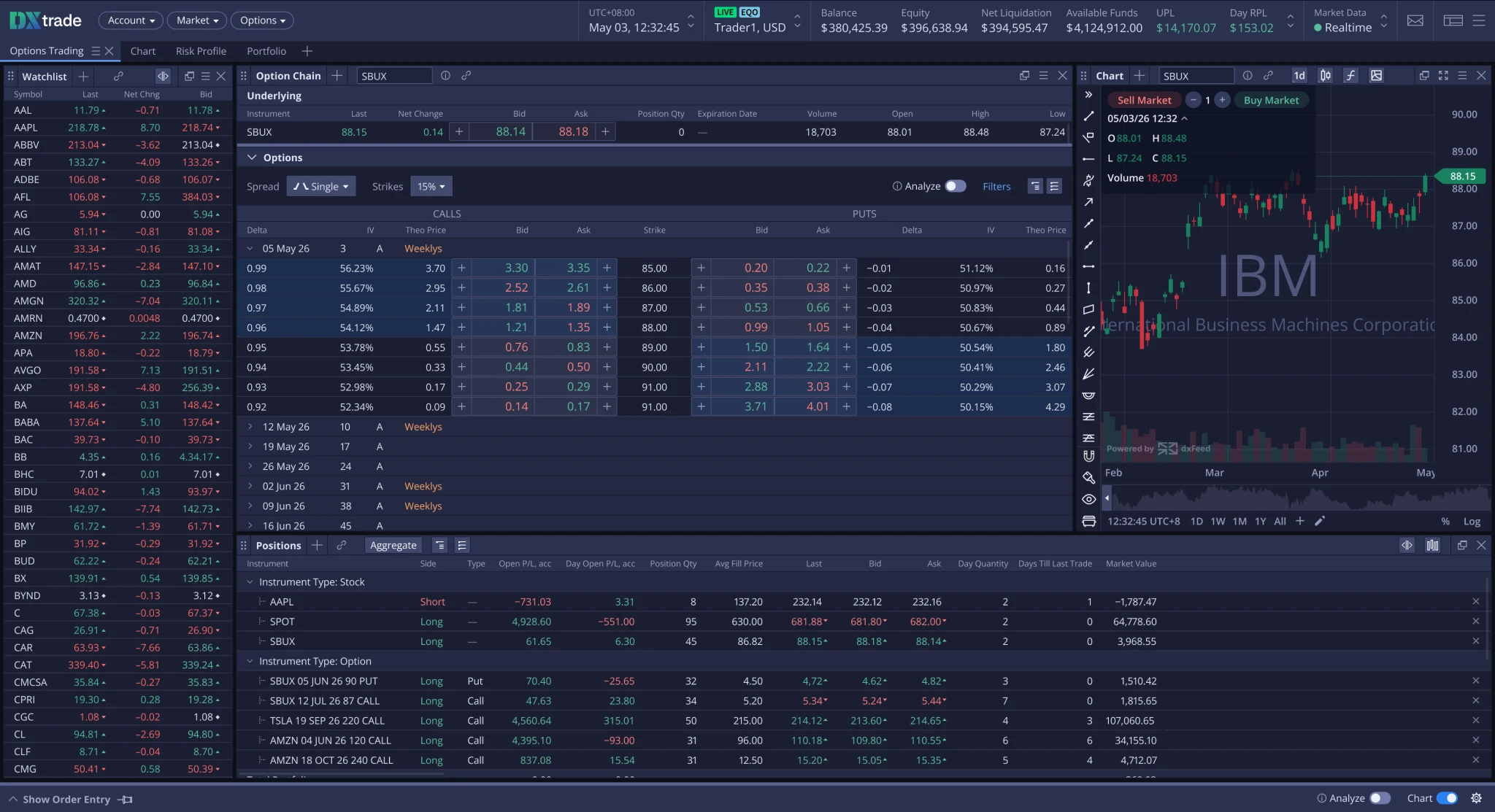

How DXtrade approaches the problem

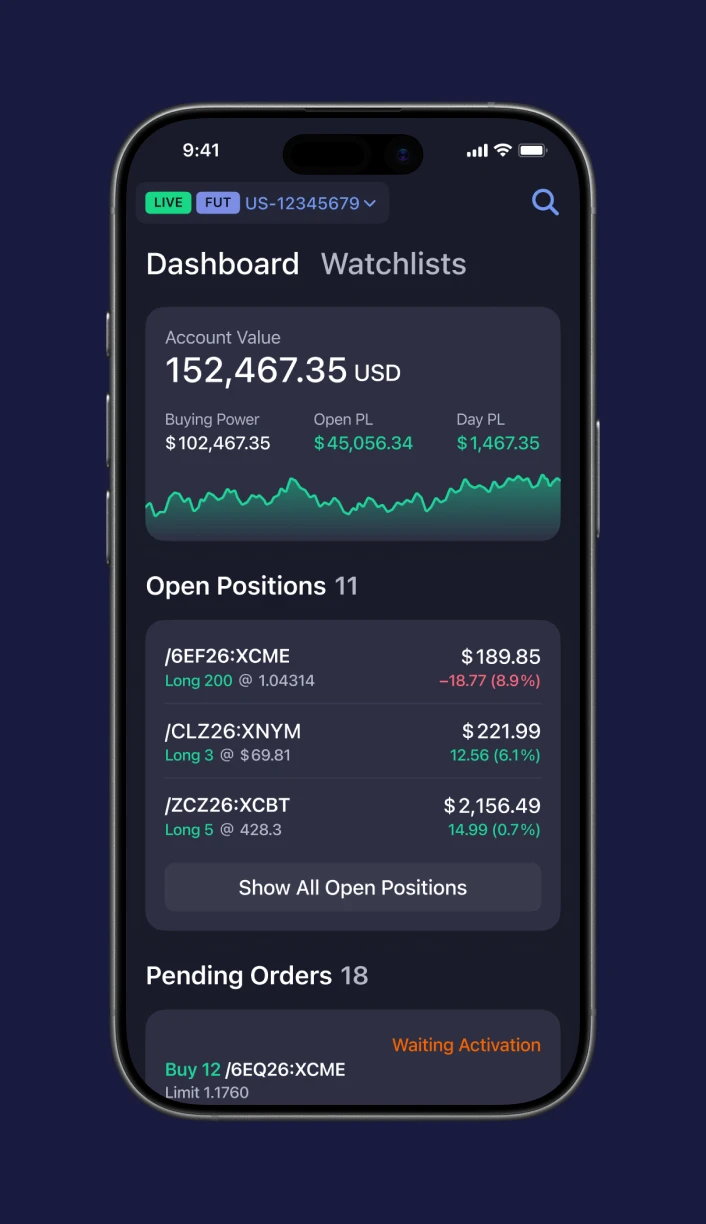

DXtrade, the Devexperts platform that runs equities and equity options alongside futures, handles all three asset classes inside one account. The order management system handles share-based and notional sizing in one fill engine, with fractional execution available where the broker enables it. Pre-allocated block orders flow through one entry point with post-trade allocation across underlying accounts. Cash and margin accounts run side by side, with PDT monitoring and Reg-T violation prevention.

The margin engine runs Reg-T and options margin on the securities side and CME SPAN on the futures side, recalculating across complex portfolios on every position change. Pre-trade validation rejects orders that violate margin rules before they reach the exchange. Post-trade monitoring drives automatic liquidation when positions breach configured thresholds, with intraday margin discounts and broker-defined liquidation levels. The Option Expiry Risk Monitor calculates the impact of assignment or exercise at defined expiration dates, an operational tool that matters more when half a broker’s volume sits inside five days of expiry.

The order book supports single through multi-leg spreads, including verticals, straddles, strangles, ratio and back spreads, calendars, diagonals, butterflies, condors, and iron condors as preset structures, with custom user-defined spreads supporting up to 40 legs on CME and equivalent strategies on ICE. The platform connects to CME and ICE for primary futures execution, with optional integration to other U.S. futures exchanges. Executing destinations include CQG and StoneX. Market data flows from dxFeed across global exchanges.

Brokers can deploy DXtrade as SaaS within weeks or take an enterprise version with deeper customization and source-code access.

Conclusion: the unified stack is now the differentiator

Most platform conversations in 2026 still treat the securities side and futures as separate problems with separate vendors. The market has moved on. Retail traders run combined futures options strategies every day, prop firms recruit on the strength of cross-asset access, the margin economics of cross-product offsets now exceed $10 billion a day at the clearinghouse level, and brokers without unified platforms watch outflows to those that have them. The brokers attracting this flow present one account, one margin number, one position view, and one strategy ticket across the securities side and the futures side. Everything else is a workaround.

Building this stack takes work: a unified OMS, multi-leg validation and fill logic that survive partial executions, a margin engine that runs Reg-T, portfolio margin, SPAN, and SPAN 2 simultaneously, symbology that translates between Globex and OSI, and lifecycle handling for assignment and exercise. Vendors have already done it. Brokers no longer have to build it themselves.

See DXtrade in action

If you are evaluating a futures and options trading platform that handles equities and equity options on the securities side together with futures inside one account, with continuous SPAN and Reg-T margining, exchange-native and user-defined multi-leg spreads, position-keeping that survives multi-leg partial fills, and a deployment timeline measured in weeks, request a demo of DXtrade.